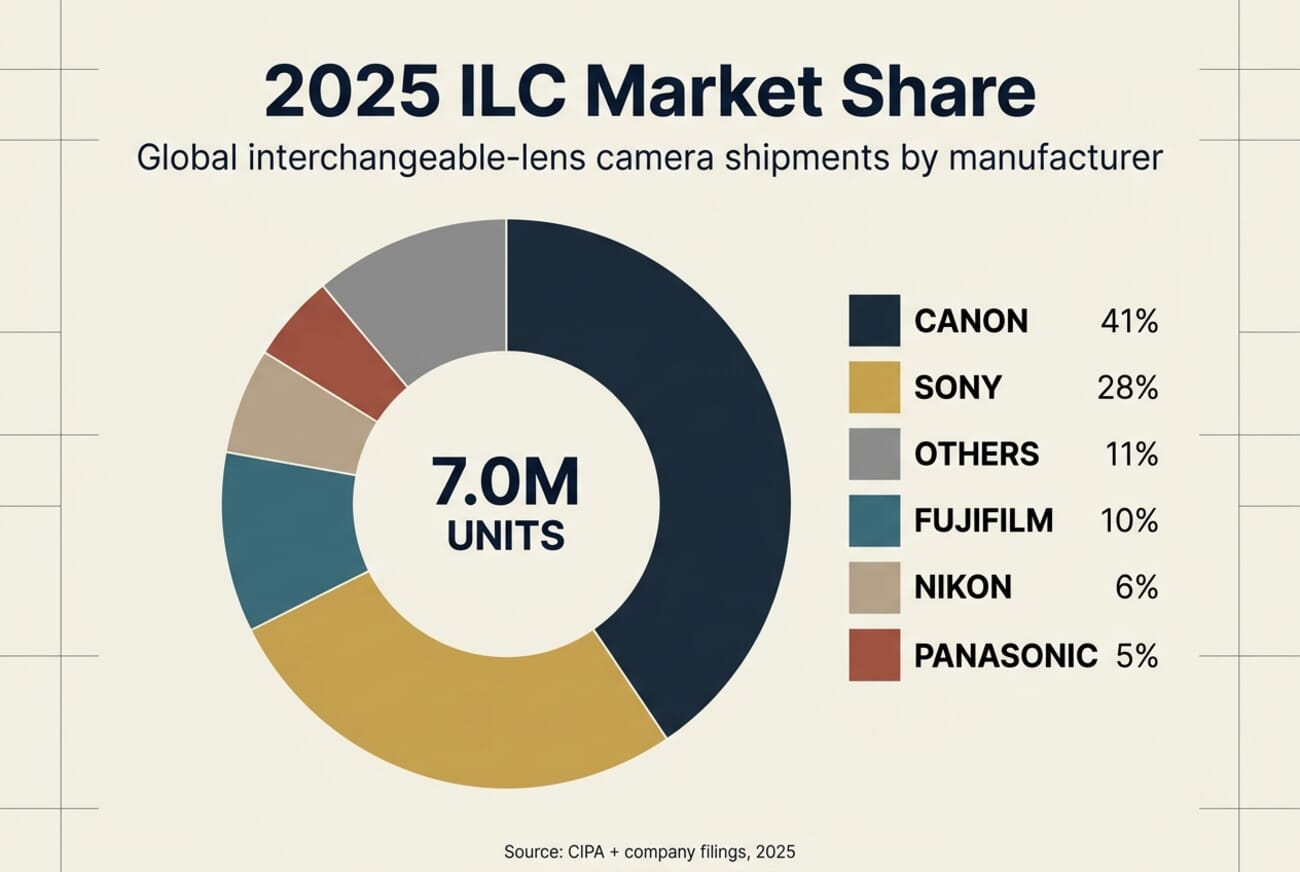

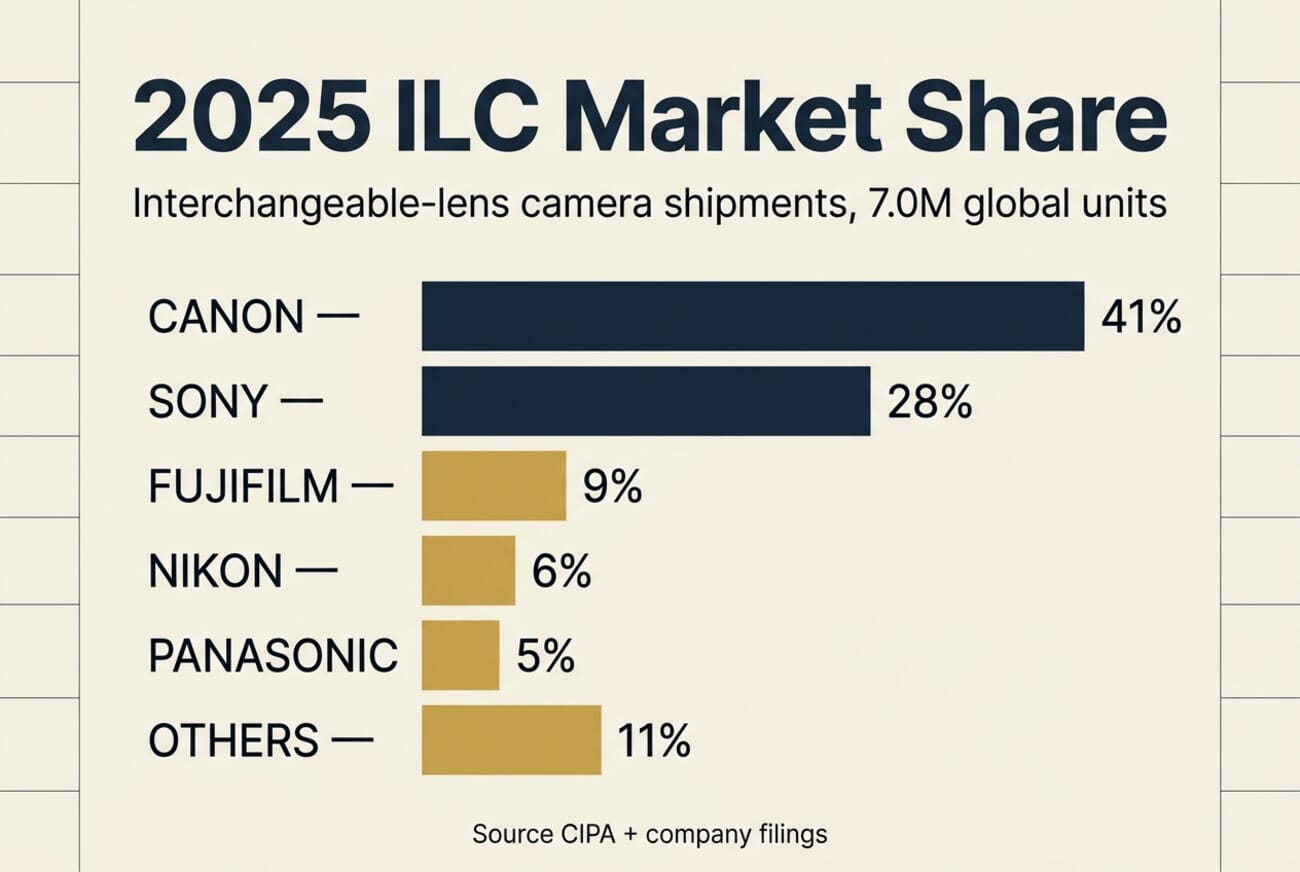

- Canon shipped an estimated 2.88 million interchangeable-lens cameras in 2025 — roughly 41% of a 7.0 million-unit global market that beat CIPA’s own forecast by 340,000 units.

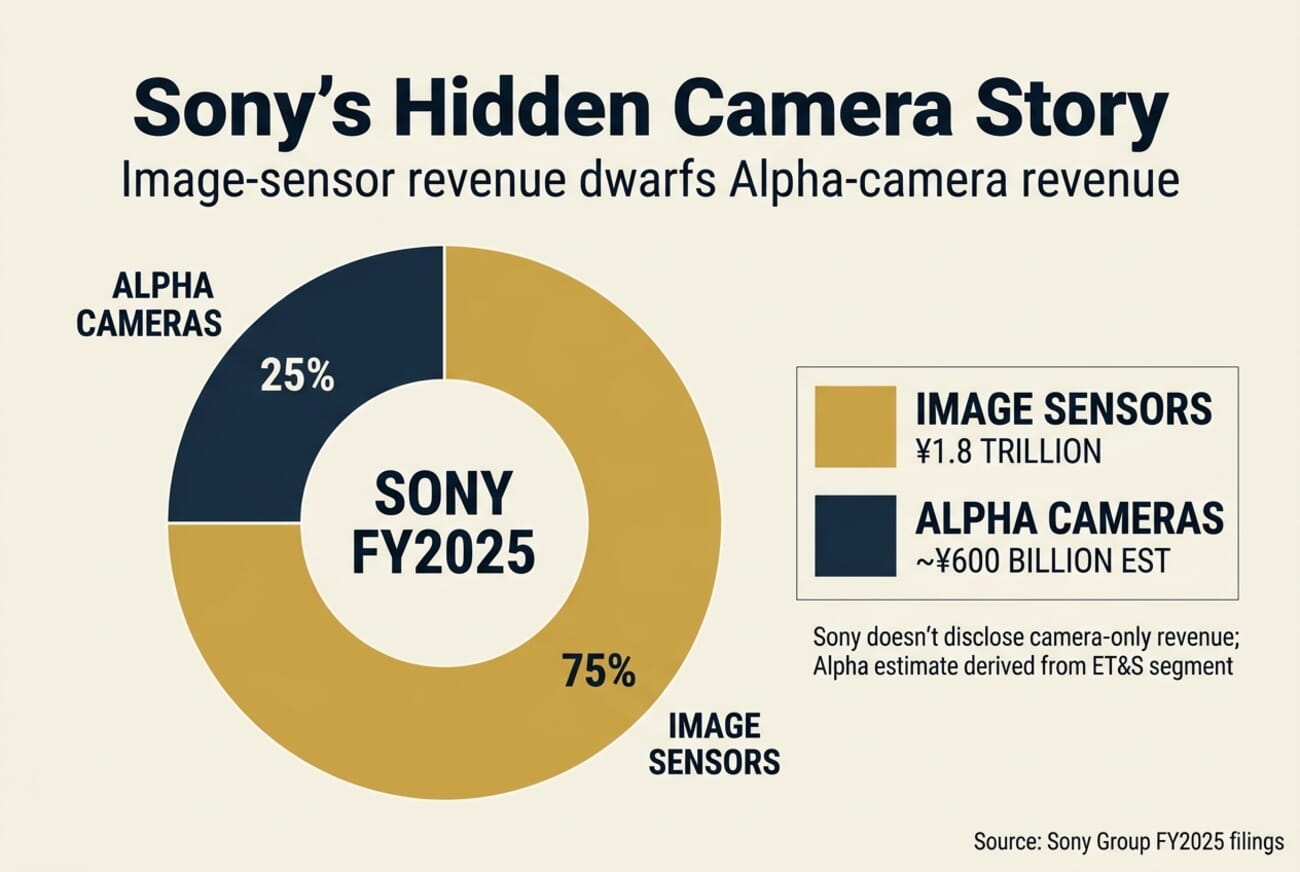

- Sony’s image-sensor business (approximately ¥1.8 trillion in revenue) is roughly three times larger than its camera-body business, which makes the Alpha camera line a strategic brand play rather than a volume race.

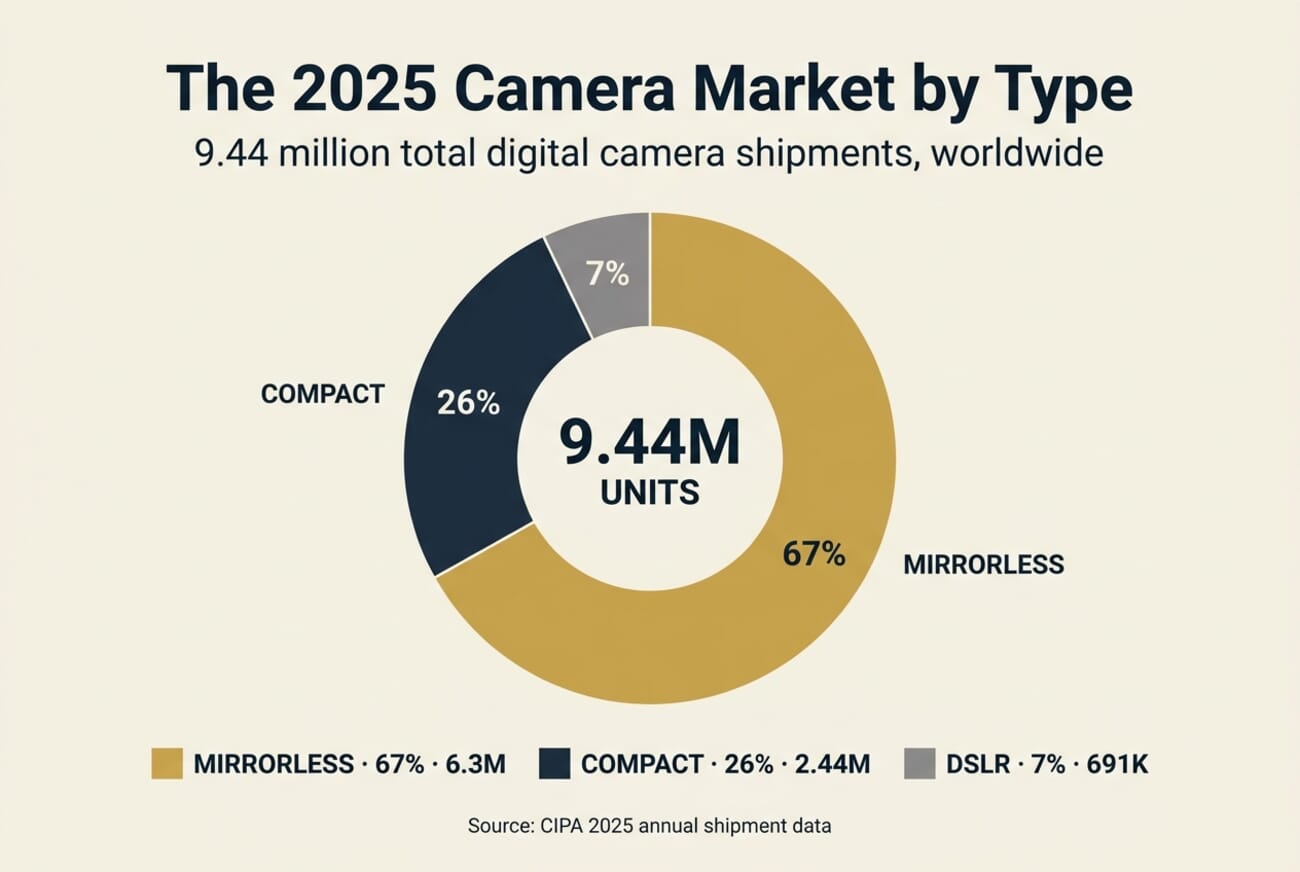

- The DSLR is functionally over: 691,000 global units shipped in 2025 (−31% year-over-year), versus 6.3 million mirrorless units — a 90/10 split that closes one of photography’s longest eras.

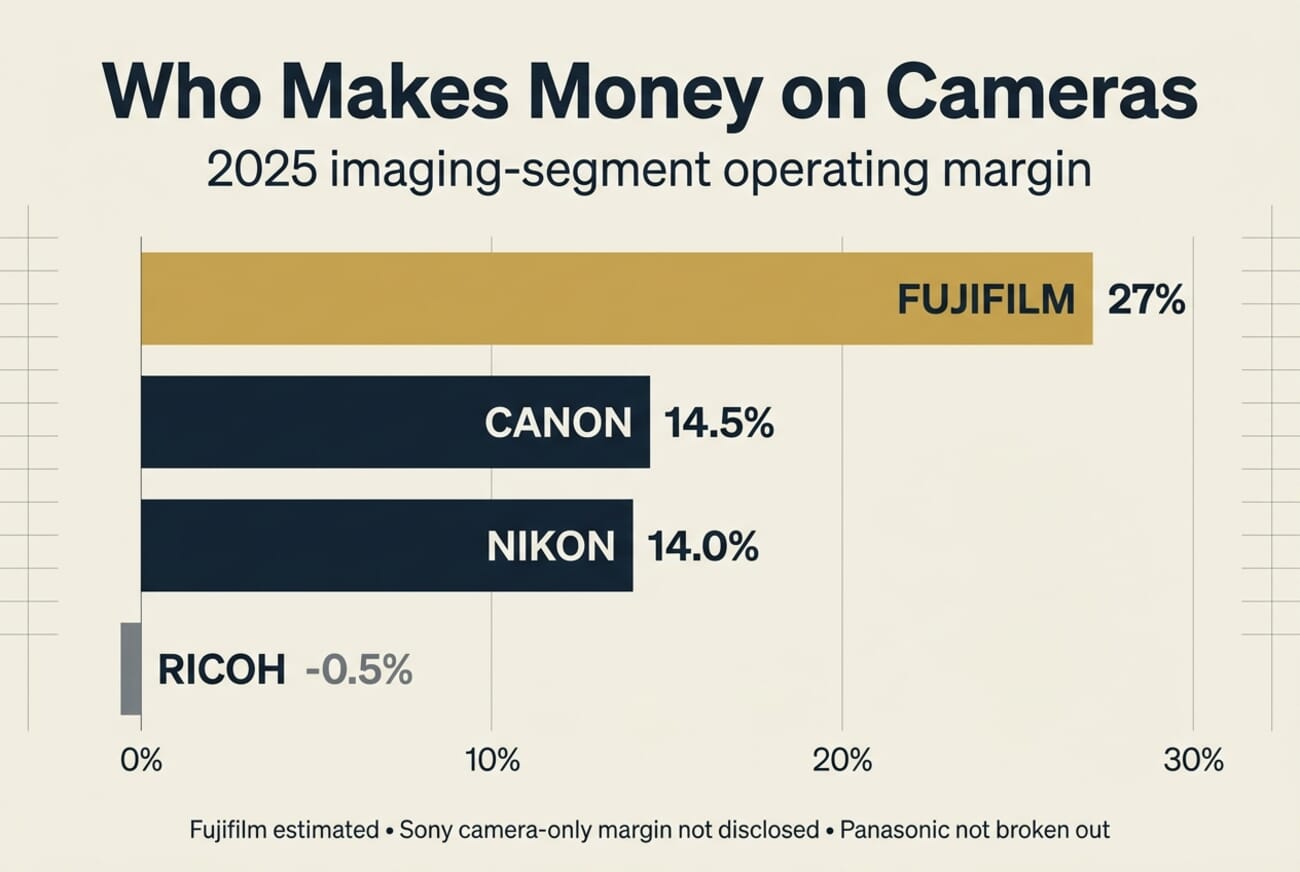

- Fujifilm runs the highest imaging-segment operating margin of any major camera maker — an estimated ~27%, nearly double Canon’s 14.5% — on the back of premium-priced X Series bodies and a sustained X100VI shortage that was a pricing-power story, not a supply-chain failure.

- CIPA’s own 2026 forecast calls for ILC units to decline 2.6% next year, with US tariffs on Japanese and Thai-built camera gear as the biggest wildcard — Canon, Nikon, and Sony all manufacture heavily in those jurisdictions.

The annual-report season for 2025 is closing out, and the camera industry’s biggest story is the quiet one: Canon now ships more interchangeable-lens cameras than every other manufacturer combined. Cross-referencing CIPA’s 2025 total shipment data against Canon’s, Sony’s, Nikon’s, Fujifilm’s, and the smaller players’ most recent filings shows a market that’s larger than expected, more concentrated than ever at the top, and — in 2026 — likely to shrink for the first time since 2022.

This piece pulls the hard numbers from each manufacturer’s public reporting, reconciles them with CIPA’s industry totals, and lays out the 2026 projection. Some of what the data reveals is obvious (the DSLR is dead), some is counterintuitive (Fujifilm makes nearly double Canon’s per-dollar profit), and one number is under-reported almost everywhere: Sony earns more selling image sensors than it does selling cameras — roughly three times more.

The 2025 Market in Hard Numbers

CIPA — the Camera & Imaging Products Association of Japan, the authoritative industry body — reported approximately 7.0 million interchangeable-lens cameras (ILCs) shipped globally in 2025. That’s up about 7% year-over-year from 6.5 million in 2024, and it beat CIPA’s own pre-year forecast of 6.66 million by more than 340,000 units. 2025 is the first two-year consecutive-gain period in digital camera shipments since 2007, before smartphones fundamentally restructured the consumer camera business.

Inside that ILC total, the mirrorless-versus-DSLR split is now decisive. Mirrorless accounted for about 6.3 million units (up ~12% YoY); DSLRs collapsed to 691,000 (down 31%). That’s a 90/10 ratio — mirrorless now represents nine out of every ten new ILCs sold worldwide, and the absolute DSLR count is a fraction of its 13-million-unit peak in 2012. The compact camera segment also posted a genuine comeback at roughly 2.44 million units (+30% YoY), with revenue up nearly 50% thanks to premium pricing on film-simulation bodies like Fujifilm’s X100 series and Sony’s ZV line. CIPA’s early-2026 numbers confirmed the DSLR’s functional end at just 35,055 shipments in a single month.

The compact resurgence deserves a closer look than it usually gets. After a decade of smartphone cannibalization, premium fixed-lens bodies found a durable niche — compacts outsold DSLRs roughly five-to-one in January 2026, driven by creator/vlogger demand for pocketable quality and the halo effect of Fujifilm’s film-simulation bodies.

Canon: The 41% Market-Share Quiet Monopoly

Canon’s FY2025 report (calendar year, Jan–Dec 2025) confirms that the imaging business unit posted a record ¥1,054.9 billion in revenue — roughly US $6.8 billion — with ¥625.5 billion from cameras specifically and ¥429.4 billion from network cameras. ILC shipments hit 2.88 million units, up 2% YoY. Segment operating profit was ¥153.1 billion at a healthy 14.5% margin.

The 2.88 million-unit figure, set against CIPA’s 7.0 million total, puts Canon at approximately 41% of global ILC shipments by units. That’s not marketing spin; it’s arithmetic. For context, Canon alone ships more cameras than Sony, Nikon, Fujifilm, Panasonic, and every smaller brand combined. The gap to #2 Sony is roughly 1:1.5, and the gap to #3 Nikon is 7-to-1 — a ratio more typical of monopoly markets than mature consumer electronics.

The product engine behind Canon’s 2025 dominance was the November launch of the EOS R6 Mark III with its 32.5MP sensor, internal 7K RAW, and 40fps burst, alongside entry-level mirrorless expansion in the R50 / R100 tier. The pipeline for 2026 is already public: the EOS R7 Mark II reportedly lands with a 39MP BSI stacked APS-C sensor — a first for Canon APS-C, and a clear signal that Canon intends to hold the creator/hybrid segment that compact full-frame bodies like Sony’s A7C II had been targeting. Canon’s FY2026 internal guidance calls for 2.95 million ILC units (about +2% YoY) and camera revenue growth of roughly 8%.

Sony: The Sensor Business Is Bigger Than the Camera Business

Sony Group’s FY2025 reporting (Apr 2024–Mar 2025) splits the imaging story across two segments. The Entertainment, Technology & Services (ET&S) segment — which houses the Alpha camera line alongside TVs, audio, and mobile — reported ¥2,409.3 billion in revenue and ¥261.1 billion in operating profit. Separately, the Imaging & Sensing Solutions (I&SS) segment — the sensor-fabrication business that supplies iPhone cameras and many of Nikon’s and Fujifilm’s sensors — reported approximately ¥1,799.0 billion in revenue with ¥261.1 billion in operating profit.

That second segment is the less-discussed part of Sony’s camera story. Sony doesn’t report Alpha-camera-only financials publicly, but the camera-body business is a fraction of ET&S — and the sensor business at ¥1.8 trillion is roughly three times larger than the entire Alpha line. In practical terms, Sony earns more money supplying the camera module inside your iPhone than it does selling α7 V bodies, and that gives Sony an entirely different incentive structure than Canon or Nikon. Premium pricing on Alpha cameras is essentially a brand-equity reinforcement; Sony isn’t under pressure to win the volume race. Sony Semiconductor’s recent reveal of the Chip-on-Wafer copper-hybrid-bonding IMX820 sensor inside the Nikon Z6III is a direct look at how deep the sensor business actually goes.

Estimated ILC share: around 28% (roughly 1.96 million units) — firmly second and well clear of Nikon. Japan BCN Awards data shows Sony holding 29.9% of the full-frame mirrorless segment specifically, though that figure is down about six points from 2024 as Nikon’s Z6III and Canon’s R5 Mark II claimed back some high-end share. The pipeline focus is the Alpha 7R VI (announced May 2026 at 66.8MP), which lands mid-FY2026 and likely anchor the full-year guidance of ¥280 billion ET&S operating profit.

Nikon: A Distant Third With Stable Revenue but Falling Profit

Nikon Corporation’s FY2025 (Apr 2024–Mar 2025) Imaging Products Business segment reported ¥295.3 billion in revenue — about US $1.95 billion — on approximately 390,000 ILC units. Segment operating profit was ¥41.3 billion at a 14% margin. Revenue grew 5.6% YoY on Z50II and Z6III demand combined with yen tailwinds, but operating profit fell 11.3% due to losses at RED Digital Cinema (post-2024 industry-strike slowdown) and impairment charges at Mark Roberts Motion Control.

At 390,000 units, Nikon is a credible #3 — but the gap to Canon is 7-to-1. Nikon’s FY2026 guidance calls for essentially flat revenue and operating profit, which is the most honest hint the company has publicly given about tariff risk. The US $4,800 rebate campaign Nikon ran in April 2026 was explicitly positioned as a window to buy before tariff-driven price hikes take effect — that’s not a sentence that appears in a flat-revenue forecast by accident.

Fujifilm: The Margin King Nobody Talks About

Fujifilm Holdings is the most interesting financial story in cameras, and it’s barely discussed. The company doesn’t disclose ILC unit shipments, which makes ranking them by volume speculative — but the imaging segment’s profit profile is extraordinary. Estimated FY2025 imaging-segment revenue is approximately ¥580 billion, operating profit about ¥155 billion. That’s roughly a 27% operating margin — nearly double Canon’s 14.5% and Nikon’s 14%.

Three things drive that margin. First, Fujifilm controls premium X-Trans sensor design and manufacturing, so they capture more of the bill of materials than manufacturers buying Sony sensors. Second, X Series bodies carry high average selling prices relative to their BOM — the X100VI’s year-long supply shortage through most of 2024 and 2025 was a pricing-power signal, not a manufacturing failure. Third, GFX medium-format is essentially a category of one at its price point, letting Fujifilm charge near-Hasselblad prices with far better economics. The interchangeable-lens Fujifilm X-E5 launched at $1,699 with the same 40.2MP sensor as the X100VI — a near-perfect case study in platform monetization.

If Fujifilm’s estimated ILC share sits somewhere between 9-12%, they make roughly as much operating profit from cameras as Nikon does while shipping substantially fewer units. That’s the quiet success story of the 2025 market.

Panasonic, OM System, Ricoh: The Long Tail

Panasonic is the most visibility-challenged player: LUMIX camera financials are rolled into a ¥3.58 trillion Lifestyle segment alongside white goods and beauty products, so the camera line is effectively invisible in their financial reporting. Global market share is estimated below 5%. Panasonic did hit a record 10% of the European full-frame market in Q1 2026 — up from 3% in 2020 — which suggests the LUMIX S series is building genuine regional share even if the total global number is modest. The special-edition Lumix S9 and 40mm f/2 S prime revealed at NAB in April fit that repositioning.

OM Digital Solutions (the former Olympus) is private since 2021. Nikkei’s 2026 industry mapping estimates CY2024 imaging revenue at ¥36.6 billion (~US $242 million) and approximately 130,000 ILC units — roughly 2% of the global market. Revenue grew 25% YoY on OM-1 Mark II and OM-5 demand, but the segment remains operating-loss at ¥-1.2 billion. The April 2026 corporate restructuring that made CEO Shigemi Sugimoto the principal shareholder is a direct bet on faster decision-making as compensation for smaller scale.

Ricoh (Pentax + Ricoh GR) reports camera revenue inside a ¥557 billion “Other” segment that also bundles industrial products, so the camera-only number isn’t isolable. The Pentax K-mount DSLR line operates at minimal volume, while the Ricoh GR III / GR IV compact line carries the business on cult demand — the recently-launched Ricoh GR IV Monochrome at $2,200 is a good example of the margin-over-volume strategy. Ricoh’s imaging segment is still operating-loss at ¥-2.9 billion, though that’s improved from ¥-5.1 billion the prior year.

What 2026 Will Likely Look Like

CIPA’s own 2026 forecast — which tends to run conservative — calls for total digital camera shipments of 9.59 million units (+1.6% YoY), but inside that total ILC units are projected to decline 2.6% to 6.82 million. Mirrorless growth is moderating as the easy wins from DSLR conversion play out, and DSLR erosion continues its march toward zero. The compact comeback is forecast to continue: +13.6% to 2.77 million units.

Three forces will shape the actual 2026 outcome. First, tariffs: proposed US duties on Japanese, Taiwanese, and Thai camera imports could push body prices up 10-25% in Canon, Nikon, and Sony’s largest single market. Retailer rebate programs have already front-loaded Q2 US demand to avoid the hit. Second, the compact market: if Fujifilm, Ricoh, and Sony sustain 30%+ YoY growth on premium fixed-lens bodies, the cross-subsidy effect on the broader imaging businesses (ASPs up, margins holding) helps all players. Third, upper-end mirrorless: Sony’s A7R VI (now official at 66.8MP), Canon’s EOS R7 Mark II, and Nikon’s next Z9 successor will compete for the $3,500-$5,000 segment that carries the industry’s margin. CP+ 2026 set an attendance record in February, and the themes from that show — sensor arms race, compact comeback, AI integration — are the themes the 2026 reports will be written against.

The base-case projection: Canon holds ~41% share, Sony holds ~28%, Fujifilm grows slightly to ~10% on X-E5 and GFX volume, Nikon holds 6% on guidance-level flat revenue, and Panasonic + OM System + Ricoh fight for the remaining 15% with margin pressure for all three. Tariff upside (for the market) goes to whoever manufactures closest to the US, which currently nobody does in meaningful volume. Tariff downside goes proportionally to everyone — but hits Nikon and Ricoh hardest because their imaging profit margins are thinnest.

What This Means If You’re Buying a Camera in 2026

The practical takeaway is simple. The camera industry has consolidated to three functionally separate tiers — volume (Canon), premium (Sony + Fujifilm), and niche (Panasonic + OM System + Ricoh) — and picking the right body is increasingly about which tier’s ecosystem matches your use case, not which brand has the best spec sheet for a single model. Canon’s volume scale means the deepest native lens lineup and broadest accessory market. Sony’s sensor lead means the most advanced autofocus and dynamic-range envelopes. Fujifilm’s margin discipline means sustained body updates at premium prices without obsolescence discounts.

For buyers specifically watching tariff news, the short window before Q3 2026 is likely the best pricing environment of the year on US-sold bodies. Rebate programs from the major brands are already signaling as much, and Q2 retailer inventory is built on pre-tariff landed cost. After that, if tariffs land as drafted, expect 10-25% headline-price increases across mirrorless ILCs — which, combined with a contracting unit market, means the 2025 pricing tier is probably the floor.

FAQ

Where do the market share numbers actually come from?

Three sources, triangulated. CIPA publishes authoritative global unit and revenue totals for ILC and compact cameras. Each manufacturer’s annual or integrated report discloses segment-level revenue, operating profit, and (for Canon) unit shipments. Share percentages are computed by dividing each manufacturer’s reported units into the CIPA global total. Where units aren’t disclosed (Sony, Fujifilm, Panasonic), estimates are derived from revenue-to-ASP ratios and cross-checked against independent research like BCN Awards Japan data.

Does Sony really earn more from image sensors than from cameras?

Yes, by a wide margin. Sony’s Imaging & Sensing Solutions segment — which sells image sensors to Apple, Samsung, and virtually every phone and camera manufacturer — reported approximately ¥1.8 trillion in revenue in FY2025. The Alpha camera line is a small fraction of the separate ET&S segment’s ¥2.4 trillion revenue. Camera-only revenue is in the low hundreds of billions of yen at most.

Why is Fujifilm’s margin so much higher than Canon’s?

Product mix plus pricing discipline. Fujifilm concentrates on premium-priced X Series APS-C and GFX medium-format bodies rather than chasing entry-level volume. The X100VI’s extended backorder period (most of 2024 and into 2025) was a signal that Fujifilm wasn’t willing to discount into demand — they let the wait list build instead. Canon spans the full price range from the ¥80,000 EOS R100 to the ¥900,000 EOS R1, which averages margins down.

Is the DSLR really dead?

Functionally, yes. 691,000 DSLR units in 2025 globally (down 31% YoY) — most of those Canon — against 6.3 million mirrorless. Nikon has effectively exited the format in practical terms. Ricoh/Pentax continues minimal K-mount production for a niche audience. At current decline rates, DSLRs will be under 300,000 units by 2027.

What’s the biggest risk to the 2026 forecast?

US tariffs on Japanese and Thai-manufactured camera gear. Canon, Nikon, Sony, Fujifilm, and Panasonic all manufacture heavily in those jurisdictions. CIPA’s own -2.6% ILC forecast doesn’t fully price in tariff escalation — if headline tariffs stick at 10-25% on camera imports, unit demand could compress further and Q3-Q4 2026 could be materially worse than the base case.

Bottom Line

2025 was the year the camera industry consolidated into a stable oligopoly. Canon owns the volume market and has the pipeline to keep it. Sony is increasingly indifferent to camera volumes because sensors pay the bills. Fujifilm built a quietly dominant margin position on premium pricing. The rest of the field is fighting for share in a market CIPA expects to contract in 2026. The buyer question for the next twelve months is whether tariffs hold and how hard — and the answer will determine whether 2026 is merely softer than 2025, or a genuine step-change to a smaller industry.

Image credit: editorial concept photography and infographics by PhotoWorkout. Market data compiled from CIPA and manufacturers’ publicly filed reports.

Primary data sources for this article:

Industry Data

- CIPA — Camera & Imaging Products Association (global shipment statistics) – Monthly and annual ILC / compact camera unit and value data; authoritative industry totals

Manufacturer Filings

- Canon Inc. — Annual Report / Investor Relations – FY2025 imaging BU revenue ¥1,054.9B, ILC units 2.88M, operating profit ¥153.1B

- Sony Group — Investor Relations Library – FY2025 ET&S and I&SS segment revenues and operating profit

- Nikon Corporation — IR Library (Financial Results) – FY2025 imaging products segment ¥295.3B revenue, 390K ILC units, ¥41.3B op profit

- Fujifilm Holdings — IR Library – FY2025 / FY2026 9-month imaging segment revenue and profit data

- Panasonic Holdings — IR Library – Lifestyle segment revenue ¥3.58T (LUMIX not broken out)

- Ricoh — Investor Relations – Other segment ¥557B (includes imaging)