- CIPA’s January 2026 data shows just 35,055 DSLRs shipped worldwide – down 36% year-over-year, with shipped value falling 45%

- Compact cameras outsold DSLRs nearly 5-to-1 (168,847 vs 35,055 units), growing 36% while DSLRs declined 36%

- Mirrorless cameras shipped 418,488 units (+16% YoY), continuing to dominate the interchangeable lens market

- CIPA forecasts 9.59 million total cameras for 2026 – just 1.6% growth, with mirrorless expected to decline 2.6% for the first time

- The Canon 5D Mark IV was just discontinued (March 2026), ending one of the most iconic DSLR lines in history

The DSLR isn’t dying. It’s already dead – the market just hasn’t finished the paperwork.

When the Camera and Imaging Products Association (CIPA) released its January 2026 global shipment data, the numbers confirmed what industry watchers have been saying for years: the DSLR era is over. Japanese manufacturers shipped just 35,055 DSLRs worldwide in January – a number so small it’s almost a rounding error in an industry that once moved 100 million cameras a year.

But this isn’t just another “DSLR is dead” hot take. We’ve compiled CIPA’s historical data, the 2026 forecast, and January’s actual shipment numbers into what we believe is the most comprehensive visual analysis of where the camera market stands right now – and where it’s headed.

If you’ve been following our initial coverage of the January CIPA data, consider this the deep dive.

The January 2026 Numbers: A Market in Transition

CIPA’s January 2026 global shipment report breaks down into three camera categories, and each tells a distinctly different story:

- DSLRs: 35,055 units shipped (-36% year-over-year), with shipped value down 45%

- Mirrorless: 418,488 units shipped (+16% YoY), value up 12%

- Compact (fixed-lens): 168,847 units shipped (+36% YoY), value up 34%

The symmetry is striking: compact cameras grew exactly as fast as DSLRs declined – 36% in each direction. One format’s loss is literally another’s gain.

But the unit numbers only tell part of the story. The 45% drop in DSLR value versus a 36% drop in units means the remaining DSLRs being shipped are cheaper models – likely inventory clearance rather than genuine demand. Meanwhile, compact cameras saw value growth (34%) nearly match unit growth (36%), suggesting consistent pricing across the segment.

Regional Lens Data Tells Its Own Story

The lens market adds another layer. According to CIPA’s January data, lenses for APS-C and Micro Four Thirds sensors grew 10% in units and 9% in value – but full-frame lenses grew just 4% in units while actually declining 5% in shipped value. This suggests the market is shifting toward smaller, lighter, more affordable systems.

The lens-to-body attachment rate also dropped from 1.62 to 1.59 year-over-year. Part of this is explained by Chinese lens manufacturers like Viltrox, Meike, and Sirui capturing market share – lenses that CIPA doesn’t track since they come from non-Japanese companies.

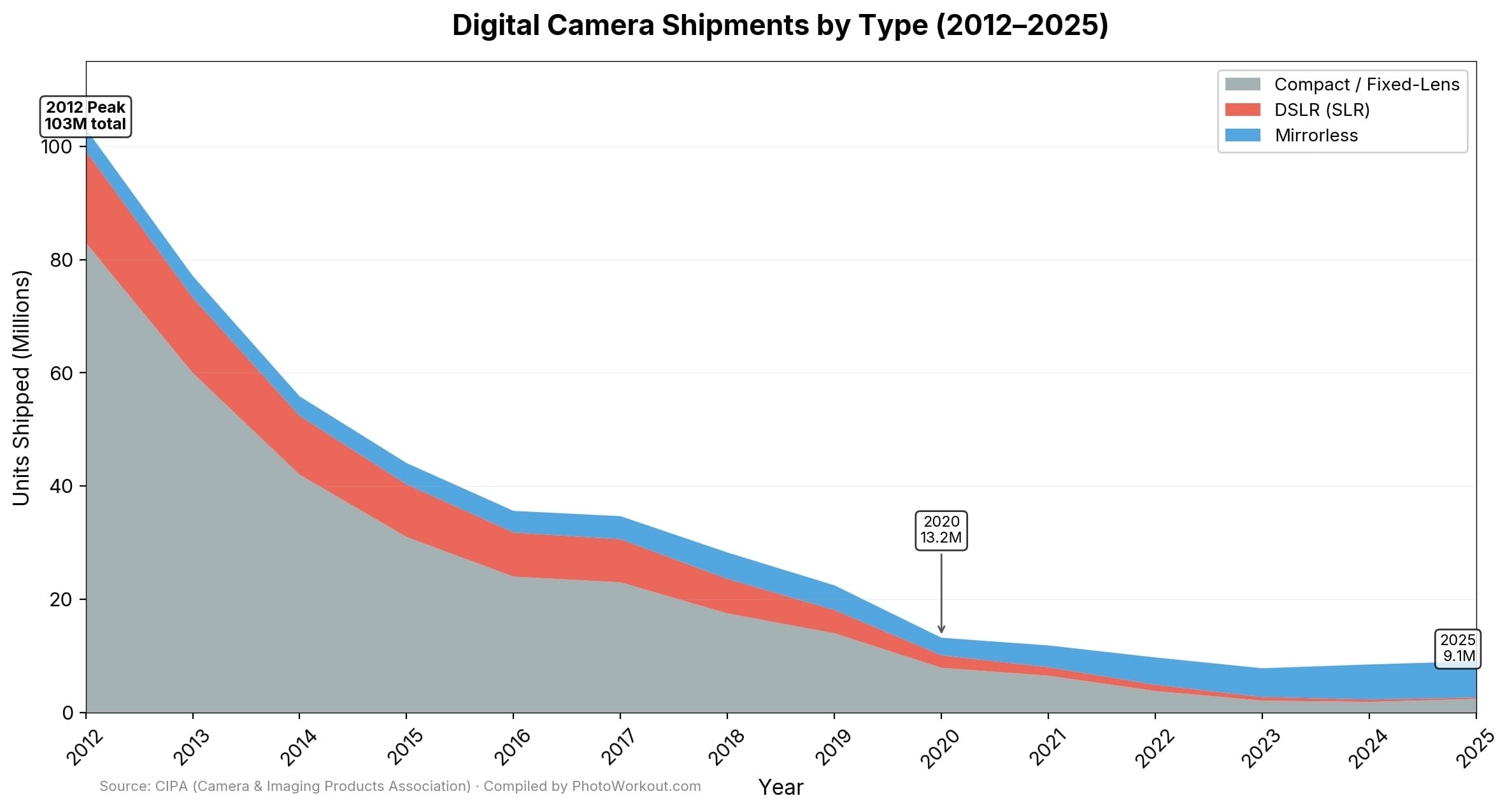

The Great Camera Shift: 14 Years of Market Upheaval

To understand where we are, you need to see where we’ve been. The camera market has undergone one of the most dramatic industry collapses in modern consumer electronics history.

Here are the key inflection points:

- 2010: The peak. Over 121 million digital cameras shipped worldwide – a number we’ll never see again. Smartphones hadn’t yet reached “good enough” camera quality.

- 2012-2013: The great collapse begins. Shipments dropped by over 35 million units in a single year – the largest year-to-year decline on record. Smartphone cameras reached acceptable quality for most consumers.

- 2017: A brief uptick in total shipments – the only increase between 2010 and 2024. It turned out to be a blip, not a trend.

- 2020: The crossover year. Mirrorless cameras outproduced DSLRs for the first time, accounting for 51.5% of interchangeable lens camera units and 65% of value. COVID accelerated the transition.

- 2024: The first genuine increase in total camera shipments since 2017. DSLR shipments hit a new all-time low of under 1 million units. Mirrorless hit a new record high.

- 2025: The best year for camera sales in over five years. Total shipments reached approximately 9.44 million units – an 11.2% increase over 2024.

That’s a 92% decline from peak to present. The camera industry didn’t just contract – it was decimated by the smartphone.

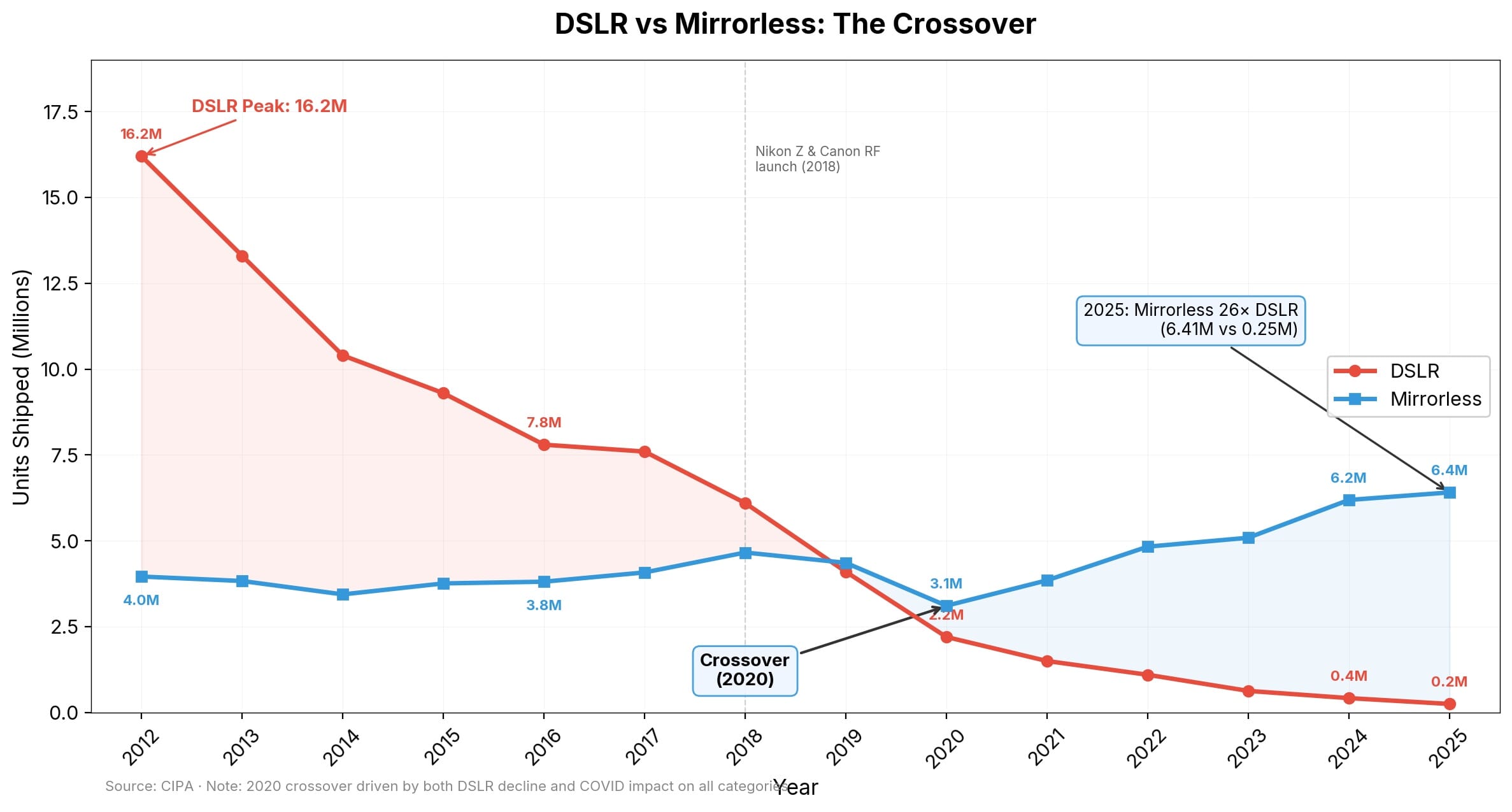

The Death of the DSLR: A Timeline

The DSLR’s decline wasn’t sudden – it was a slow, methodical wind-down as every major manufacturer shifted resources to mirrorless systems.

The key milestones in the DSLR’s decline:

- 2012: DSLR shipments peak at approximately 16.2 million units. This was the golden age.

- 2013-2017: Steady annual declines as smartphones improved and mirrorless systems gained credibility. Canon, Nikon, and Sony continued releasing new DSLRs, but the writing was on the wall.

- 2018: The turning point. Nikon launched the Z mount system. Canon introduced the RF mount. Both signaled their mirrorless future. Sony had been all-in on mirrorless since the A7 launch in 2013.

- 2020: Nikon released the D6 – its last new DSLR. Nikon also discontinued entry-level DSLRs including the D3500 and D5600. Mirrorless officially overtook DSLR in shipments.

- 2021: Sony stopped selling A-mount DSLR-style cameras entirely, going mirrorless-only. Canon confirmed the EOS-1D X Mark III would be its final flagship DSLR.

- 2022: Both Canon and Nikon confirmed they had ended DSLR R&D. New development would focus exclusively on mirrorless systems.

- 2024: Annual DSLR shipments fell below 1 million units for the first time. Only Ricoh (Pentax) maintained any meaningful DSLR involvement.

- 2025: DSLR shipments fell to approximately 691,000 units for the full year – a 31% decline from 2024. The Canon 5D Mark IV was officially discontinued, ending one of photography’s most iconic camera lines after 21 years.

- January 2026: Just 35,055 DSLRs shipped globally. At this rate, full-year DSLR shipments could fall below 400,000 units.

The DSLR isn’t being killed – it’s being abandoned. No new models are coming. No new R&D is happening. The remaining shipments are existing inventory and the handful of models still technically in production.

Mirrorless: The Dominant Force (With a Warning Sign)

Mirrorless cameras now completely dominate the interchangeable lens market. The 418,488 units shipped in January 2026 represent a 16% year-over-year increase, and mirrorless accounts for the overwhelming majority of all interchangeable lens camera shipments.

But here’s where it gets interesting: CIPA’s own 2026 forecast, released in February at CP+ in Japan, predicts a 2.6% decline in mirrorless shipments for the full year – from approximately 7.0 million units in 2025 to 6.82 million. If the forecast holds, 2026 would be the first year mirrorless shipments have declined since the COVID dip in 2020.

What does this mean? Not that mirrorless is in trouble – but that the interchangeable lens camera market may be reaching its natural ceiling. The photographers who want dedicated cameras already have them. Growth now depends on upgrades and replacements, not new converts.

The sensor size data reinforces this: 302,607 APS-C and Micro Four Thirds cameras shipped in January versus 150,936 full-frame or larger bodies. The market is clearly gravitating toward smaller, lighter, more affordable camera systems rather than premium full-frame setups.

The Compact Camera Comeback

The most surprising story in the January data is the continued rise of compact cameras. At 168,847 units shipped (+36% YoY), the compact segment is growing faster than any other camera category.

CIPA’s full-year forecast projects 2.77 million fixed-lens cameras for 2026 – a 13.6% increase over 2025’s 2.44 million. That’s strong growth, though notably slower than 2025’s 29.6% compact surge.

Several factors are driving the revival:

- Premium compacts: The Fujifilm X100VI and Ricoh GR IIIx have become status symbols as much as cameras. They’re perpetually backordered and command premium prices.

- Retro trend: Young buyers are gravitating toward dedicated cameras as a counter-trend to smartphone photography. The Yashica Tank and Canon’s retro concept shown at CP+ 2026 confirm manufacturers are leaning into this.

- Content creators: Vloggers and social media creators want a dedicated camera that’s more portable than a mirrorless system but produces better results than a phone.

- Digital minimalism: There’s a growing movement of people who want a camera that’s just a camera – no notifications, no social media, no distractions.

Canon has responded by increasing compact camera production by 50%. But even Canon’s leadership has been cautious, publicly questioning whether the compact boom is sustainable or a temporary trend.

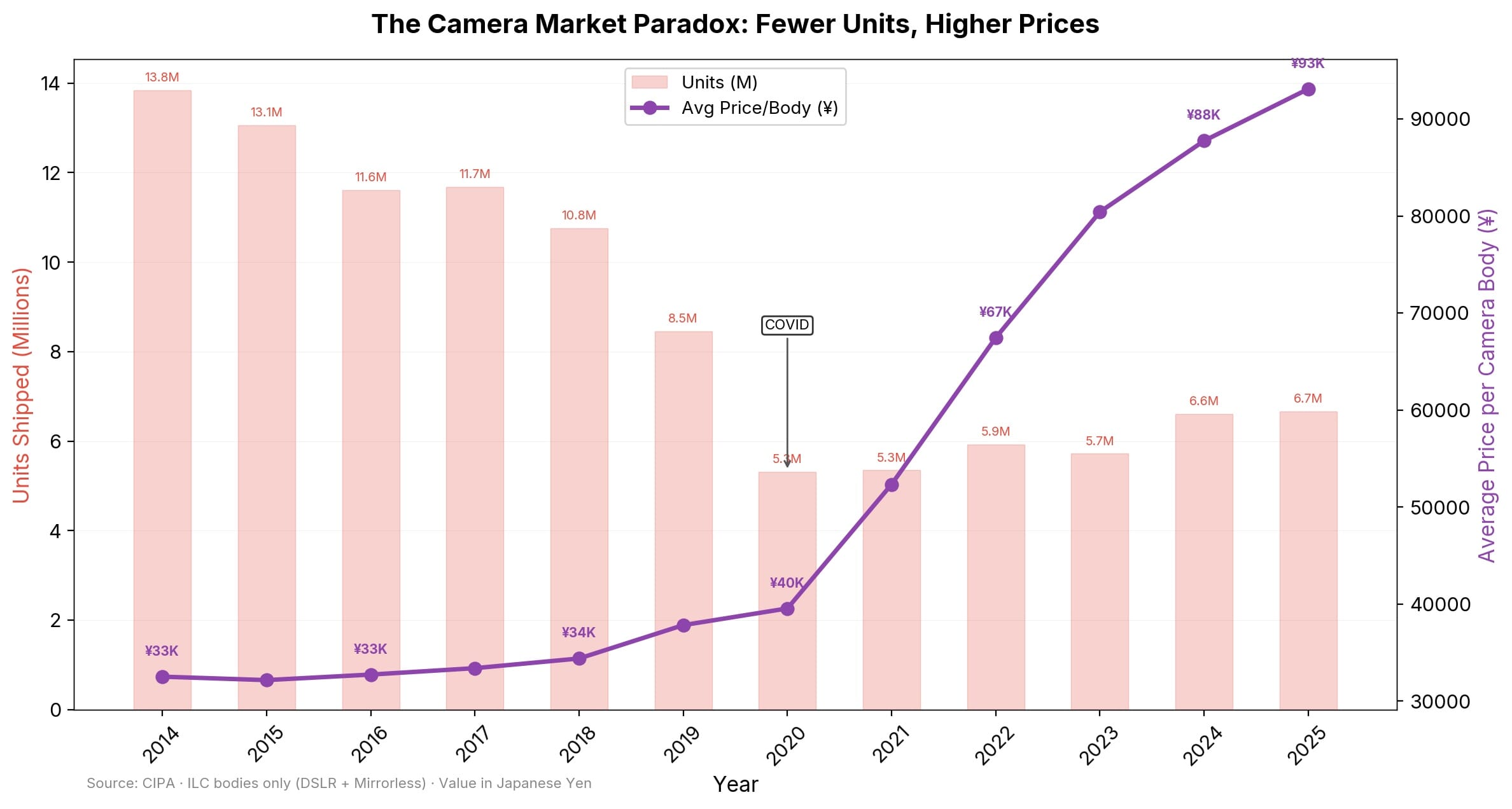

The Camera Market Paradox: Fewer Units, Higher Value

Here’s the part most coverage misses: the camera industry is actually doing better financially than the unit numbers suggest.

In 2010, over 121 million cameras shipped worldwide. In 2026, CIPA forecasts approximately 9.59 million. That’s a 92% decline in volume. But the total market value hasn’t collapsed nearly as dramatically because the average selling price of a camera has increased significantly.

Why? The cheap point-and-shoot cameras that dominated in 2010 are gone – smartphones replaced them entirely. What’s left is primarily:

- Professional and enthusiast mirrorless bodies ($1,000-$6,500)

- Premium compact cameras ($400-$1,600)

- High-end lenses ($500-$3,000+)

The camera industry has essentially shed its low-margin, high-volume consumer business and consolidated around high-margin, low-volume enthusiast and professional products. Canon, Nikon, and Sony are all reporting strong revenues despite selling a fraction of the cameras they once did.

CIPA’s 2026 forecast of 9.59 million units at 101.6% of 2025 volume suggests the industry believes it has found its floor – or close to it. The camera market isn’t going to grow dramatically, but it’s not shrinking anymore either (DSLR excepted).

What This Means for Photographers

Data is useful, but the question most photographers are asking is practical: what should I actually do with this information?

If You Shoot DSLR

Your camera still takes great photos. The sensor and optics in a Nikon D850 or Canon 5D Mark IV are still excellent. But you should be realistic about the future:

- No new bodies are coming. What exists today is what you’ll have. Plan accordingly.

- Used DSLR gear is a bargain. If you’re happy with DSLR shooting, now is the best time in history to buy used DSLR bodies and lenses. Prices are falling fast as photographers upgrade to mirrorless.

- Lens ecosystems will be supported for years. Canon EF and Nikon F lenses work beautifully on mirrorless bodies via adapters. Your glass investment isn’t wasted – it’s a bridge to mirrorless when you’re ready.

- Service and repair will eventually become difficult. As parts become scarce, maintaining DSLR bodies will get harder and more expensive. This is a 3-5 year concern, not an immediate one.

If You’re Buying Your First Camera

Buy mirrorless or a premium compact. There’s no reason to start a new DSLR system in 2026. The best cameras for beginners are all mirrorless now, and even budget options like the Canon EOS R50 or Nikon Z50 II outperform most DSLRs in autofocus, video, and features.

If you mainly shoot stills and want the simplest possible experience, a premium compact like the Fujifilm X100VI or Ricoh GR IIIx might be all you need – though good luck finding one in stock.

If You’re a Working Professional

The transition is already done for most pros. The Sony mirrorless lineup, Canon R system, and Nikon Z system all offer professional-grade bodies that exceed DSLR capabilities in nearly every metric. Eye-detection AF alone is worth the switch.

The APS-C vs full-frame data is worth noting: the majority of interchangeable lens cameras shipped are now APS-C or Micro Four Thirds, not full-frame. For many professionals, the smallest full-frame cameras or even APS-C bodies offer everything needed at lower weight and cost.

The 2026 Outlook: Stability, Not Growth

CIPA’s full-year 2026 forecast paints a picture of a market that has found equilibrium:

- Total cameras: 9.59 million units (101.6% of 2025)

- Interchangeable lens cameras: 6.82 million units (97.4% of 2025 – slight decline)

- Fixed-lens cameras: 2.77 million units (113.6% of 2025 – strong growth)

- Interchangeable lenses: 10.51 million units (99.1% of 2025 – essentially flat)

The 1.6% overall growth is modest compared to 2025’s 11.2% surge, but CIPA is essentially saying: the market has stabilized. The smartphone-driven collapse is over. What’s left is the core market – people who want dedicated cameras for reasons smartphones can’t replace.

The compact camera forecast is the most bullish segment at 13.6% growth. But even CIPA seems uncertain whether this is sustainable – as Canon’s own leadership has publicly questioned whether the compact trend is a real boom or a bubble.

The Bottom Line

Is the DSLR dead? Yes. Not “dying” – dead. When your biggest manufacturer discontinues its most iconic model, when global shipments are measured in tens of thousands rather than millions, when zero companies are investing in new development – that’s not decline. That’s extinction in progress.

But the camera industry itself? It’s healthier than the doom-and-gloom narrative suggests. Fewer cameras are shipping, but each one is more valuable. Mirrorless systems are mature and capable. Compact cameras are finding a new generation of buyers.

The 9.59 million cameras CIPA projects for 2026 won’t make headlines like the 121 million that shipped in 2010. But they’re being bought by photographers who genuinely want them – not consumers who didn’t know their phone could take a picture.

And that might be the healthiest thing to happen to the camera industry in decades.

This analysis draws on official CIPA shipment data, industry reporting, and manufacturer announcements.

Official Data

- CIPA Digital Camera Statistics – Official CIPA production and shipment data for digital cameras and interchangeable lenses

- CIPA 2026 Shipment Forecast Press Release – CIPA's official 2026 forecast released February 26, 2026 at CP+ Japan

Industry Coverage

- CIPA Data for January 2026 – Nikon Rumors – Detailed analysis of January 2026 CIPA shipment data by ZoetMB

- DSLRs on the Brink – Digital Camera World – DCW coverage of January 2026 CIPA compact vs DSLR shipment data

- CIPA 2026 Predictions – Digital Camera World – Coverage of CIPA's full-year 2026 camera shipment forecast

- Compact Cameras Outsell DSLRs Nearly 5 to 1 – PodcastVideos – Analysis of January 2026 compact camera vs DSLR sales data

- Digital Camera Shipments Increased for First Time Since 2017 – PetaPixel – Historical CIPA data analysis showing long-term camera market trends

- January CIPA Data – Photo Review Australia – Regional breakdown and lens attachment rate analysis

PhotoWorkout is reader-supported. Some links in this article are affiliate links – if you purchase through them, we earn a small commission at no extra cost to you.

Related Articles

Get the Weekly Photography News Digest

Join photographers who get our top stories delivered every Monday morning. No spam, unsubscribe anytime.