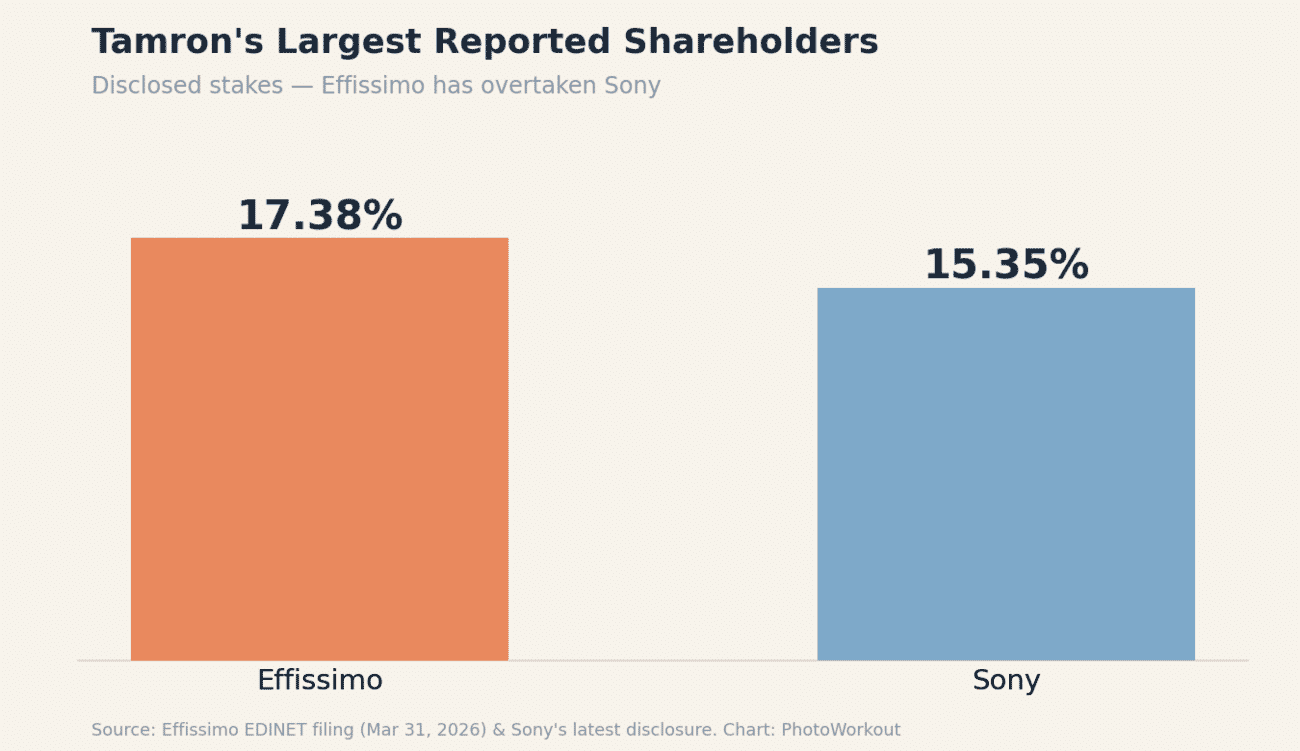

- Effissimo Capital Management now reports a 17.38% stake in Tamron — overtaking Sony’s 15.35% to become the lens maker’s largest disclosed shareholder, per a regulatory filing dated March 31, 2026.

- Effissimo is a Singapore-based investment manager led by Japanese executives, known for governance-focused activism (most famously at Toshiba). It describes the Tamron holding as a “pure investment” — there is no disclosed takeover bid or board challenge.

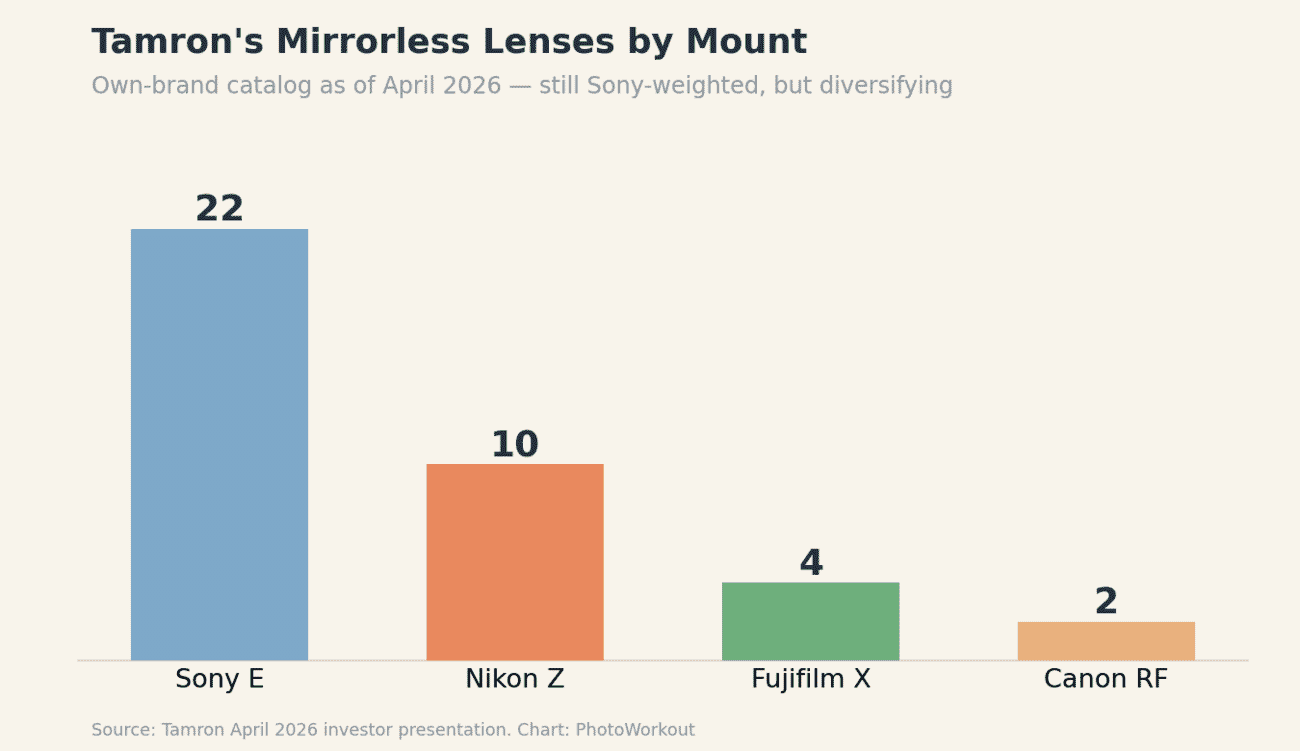

- Sony still matters a lot: it remains a major shareholder, accounts for about 23% of Tamron’s sales, and Sony E-mount is by far Tamron’s biggest mirrorless lens catalog (22 lenses vs 10 for Nikon Z).

- Tamron’s push beyond Sony E-mount (into Nikon Z, Fujifilm X and Canon RF) was already underway before this — don’t credit Effissimo for it. The most likely near-term effect is more pressure on dividends and capital efficiency.

- For current Tamron owners: nothing changes today. There’s no evidence existing lenses will lose support. The forward-looking scenarios below are analysis, not confirmed plans.

One of the most important names in third-party lenses just had a quiet but meaningful change at the top of its shareholder register. Effissimo Capital Management has overtaken Sony to become Tamron’s largest reported shareholder — and because Sony has been so closely tied to Tamron’s identity in the mirrorless era, photographers have reason to pay attention. Tamron makes the glass a huge number of us actually shoot with, from the ubiquitous 28-75mm f/2.8 to the do-everything 35-150mm, so who steers the company matters.

Before the speculation runs ahead of the facts, here’s the important part: this is a shareholding change, not a takeover. Let’s walk through exactly what happened, who Effissimo is, why Sony’s role mattered, and what it could — and could not — mean for the lenses you buy.

The Numbers: A New Largest Shareholder

According to a Japanese regulatory filing, Effissimo reports 29,691,800 Tamron shares — 17.38% of the company, measured as of March 31, 2026 and filed on April 7. Sony’s latest disclosed position was 25,038,000 shares, or 15.35%. That puts Effissimo roughly 4.65 million shares ahead, and the crossover appears to have happened back around February 9, 2026.

One nuance worth being precise about: Effissimo’s filing notes that 29,691,000 of those 29,691,800 shares are held under discretionary investment agreements — meaning Effissimo is the investment manager reporting the largest aggregate position, rather than the outright beneficial owner of every share. That doesn’t erase its influence; a 17.38% block still carries real weight in shareholder votes and management discussions. But “owner” is shorthand, and the distinction matters.

Who Is Effissimo?

This is where early reports often get it wrong, so let’s be exact: Effissimo is a Singapore-based investment manager led by Japanese executives and known for activist positions in Japanese companies — not a “private Japanese firm.” Founded in 2006 by former colleagues of the well-known Japanese activist Yoshiaki Murakami, it takes large stakes in companies it sees as undervalued and pushes on governance, board accountability, capital allocation and shareholder returns.

Its most famous campaign was at Toshiba: in 2021, shareholders backed an Effissimo proposal for an independent investigation, which concluded that Toshiba and government officials had improperly pressured some investors. That cemented Effissimo’s reputation as a serious force in Japanese corporate governance. Crucially, though, the firm currently lists its Tamron holding as a “pure investment,” and there is no disclosed board nomination, shareholder proposal, governance demand, or acquisition approach at Tamron. Anyone telling you a takeover or breakup is coming is speculating.

Why Sony Mattered to Tamron

Sony’s importance went well beyond its share rank. Tamron reports that sales to Sony Group companies were about 23.1% of its consolidated net sales in 2025 — Sony is a major customer, not just an investor, and Tamron itself flags that customer concentration as a business risk it wants to reduce. There’s a platform story too: Sony’s decision in 2011 to disclose basic E-mount specifications to licensed manufacturers helped create the broad third-party ecosystem we enjoy today, and Tamron welcomed it. The result is a lens catalog still heavily weighted toward Sony E-mount.

To be clear about what the evidence does and doesn’t show: Sony and Tamron have deep equity ties, a big customer-supplier relationship and strong E-mount platform ties. There’s no public evidence that Sony directed Tamron’s product roadmap, and Sony has not disclosed selling its stake — it remains a major shareholder and partner.

Tamron Was Already Moving Beyond Sony

Here’s the part that keeps the story honest: Tamron’s diversification beyond Sony E-mount started before Effissimo became the largest shareholder. The company has expanded into Nikon Z, Fujifilm X and Canon RF, said it planned more than 10 own-brand lens launches in fiscal 2026, and explicitly described moving away from its old “Sony E-mount first, adapt later” pattern toward launching across multiple mounts at or near the same time. We covered that shift when Tamron ditched its “Sony first” strategy. So while it’s tempting to connect the dots, this strategy predates the ownership change — Effissimo shouldn’t be credited with causing it.

What It Could Mean for Photographers

Everything below is analysis, not confirmed plans. The most plausible near-term effect is financial: activist managers tend to push for higher dividends, share buybacks and better capital efficiency. Tamron did announce on June 16, 2026 that it was raising its projected annual dividend from ¥37 to ¥51 per share, targeting a 60% payout ratio from fiscal 2027 (up from 40%), and outlining roughly ¥18 billion in additional shareholder returns through 2029. Those moves are the kind of thing an activist would applaud — but Tamron did not attribute them to Effissimo, so we shouldn’t imply it caused them.

Beyond that, a few scenarios are worth watching. Tamron may gain a bit more strategic distance from its closest camera-industry partner, reinforcing decisions made on demand and profitability rather than relationship. That could support faster multi-mount expansion — more simultaneous Sony E and Nikon Z launches, more Canon RF glass, a bigger Fujifilm X lineup — though a shareholder change can’t override camera makers’ licensing rules or autofocus negotiations. The risk to monitor is the flip side of bigger payouts: if higher shareholder returns ever came at the expense of optical R&D, autofocus development, firmware support or service, that would matter to us — so future R&D and capital-spending disclosures will tell us more than the shareholder ranking alone. And yes, an activist with 17.38% would have sway in any future transaction, but there is no bidder, tender offer or sale process on the table; an acquisition is purely speculative today.

The Tamron Lenses That Made Its Name

Whatever happens in the boardroom, Tamron’s reputation rests on glass that punches above its price. The Tamron 28-75mm f/2.8 Di III VXD G2 is the everyday standard zoom that arguably defined the brand’s mirrorless era, and the ambitious 35-150mm f/2-2.8 Di III VXD is a one-lens-does-most flagship with no real equivalent from the camera makers. On APS-C, the 17-70mm f/2.8 Di III-A — now available for Fujifilm X as well as Sony — is one of the best single-lens travel kits going. For the wider picture, see our roundup of the best Tamron lenses and our guide to mirrorless lens mounts if you’re weighing which system to buy into.

Frequently Asked Questions

Did Sony sell its Tamron stake?

No. There’s no filing showing Sony sold. Effissimo’s reported stake simply grew past Sony’s disclosed 15.35%. Sony remains a major shareholder, customer and ecosystem partner.

Is Tamron being taken over?

There’s no evidence of it. Effissimo lists the holding as a “pure investment,” with no disclosed bid, tender offer or board challenge. Any takeover talk is speculation at this point.

Will Sony E-mount lenses lose support?

Nothing suggests that. Sony E remains Tamron’s biggest catalog and a huge share of its sales. Existing lenses keep their firmware and service; this filing changes none of that today.

Should this change what lens I buy?

No. Buy the lens that fits your camera and budget. If anything, Tamron’s multi-mount push (already underway) means more options across Nikon Z, Fujifilm X and Canon RF over time.

The Bottom Line

The defensible read is straightforward: Tamron now has a governance-focused investment manager as its largest reported shareholder, at a moment when the company is broadening beyond Sony E-mount and raising shareholder returns. That’s strategically interesting — but it isn’t proof of a takeover, a breakup, an anti-Sony pivot or any change to the lenses you already own. The most likely near-term story is sharper attention to capital efficiency alongside the multi-mount strategy Tamron had already chosen. Watch for whether Effissimo’s stated purpose stays “pure investment,” whether Sony’s stake moves, and — most useful of all — what Tamron’s future R&D and product cadence actually look like.

Figures and quotes are drawn from regulatory filings, Tamron's own disclosures and the reporting below.

Image Sources

- Conceptual hero, shareholding chart, mount chart and pin — PhotoWorkout – Charts built in-house from the filings above